The flowers and trees are beginning to bloom around Kansas City, and boy, do we feel like we've earned it. Every spring brings with it a promise of warmer weather and fresh starts. But this year, the new beginning for our social lives and the growing warmth of the economy is far more exciting than the prospect of fewer coats or gorgeous cherry blossoms.

In this quarter's newsletter, we take a step back from the nuts-and-bolts of corporate earnings, interest rates, and market volatility to focus on a few recurring topics of client/advisor conversations. Call it a 'Letters to the Editor' edition.

First Up:

Our newsletter in January covered inflation in considerable detail, but inflation concerns from clients and advisors alike have continued to surface. For that reason, we have concluded that quarterly updates on the state of inflation are probably warranted. After all, the inflation drivers in 2021 should paint a clear picture of what's working in the economy. To that end, we will provide a brief review of the current state of inflation and the stated preferences of policymakers. (Check out last quarter's newsletter for an inflation primer)

Secondly:

You would have to be living under a proverbial rock to not have heard that the national housing market is Hot Hot Hot. It seems that everybody we talk to these days expresses their disbelief about pricing trends and buyers' behavior. In some cases, disbelief is often accompanied by anxiety about a potential repeat of the 2007 financial crisis. We will review housing supply/demand dynamics and draw a few distinctions and similarities with the last great housing boom.

If you have any questions or concerns, we're here to address them at any time. Please do not hesitate to reach out.

- Kyle

Inflation

Supply chain chaos, transportation costs, and commodities in short supply drove inflation to multi-decade highs in the first quarter. Those woes ricocheted through the economy in the form of dramatically higher copper/lumber/grain prices, new car and home appliance deliveries being pushed out months due to semiconductor/parts shortages, packages delayed, and even panic in the restaurant business due to a lack of single-serve ketchup packets. No matter where you look, readings on wholesale prices have increased dramatically since the beginning of the pandemic.

Globalized supply chains tend to operate on a 'just-in-time' basis. As in: "receive parts just in time to manufacture a car/refrigerator/Tonka truck" or "get a shipment of lumber just in time to build that house." The coupling of just-in-time accounting and globalization over the past 40 years allowed manufacturers to operate more efficiently, which boosted margins and earnings. The pandemic made a complete and utter mess out of that symbiotic system. And while it will take time to put the pieces back together, they will eventually recover as the pandemic abates.

As for commodity prices, there is an old saying that is useful in a time like this "The cure for high prices is high prices." In other words – if prices are high for a commodity, then businesses are incentivized to produce more of that commodity; eventually, more supply will come onto the market and send prices lower. Again, boosting individual commodities supplies takes varying amounts of time, but prices typically react negatively to increased supply.

The critical assumption in each of the analyses above is that the pandemic and its impact on prices will recede, and prices will revert lower. The expectation for 'temporary' or 'transient' increases in prices is an integral one for the trajectory of interest rate policies from global central banks.

In the most recent meeting of the Federal Open Market Committee (rate-setting body of the Federal Reserve), Chair Jerome Powell reiterated that short-term supply/pandemic impacts would not yield sustained inflation.

"…we could also see upward pressure on prices if spending rebounds quickly as the economy continues to reopen, particularly if supply bottlenecks limit how quickly production can respond in the near term. However, these one-time increases in prices are likely to have only transient effects on inflation."

The Federal Reserve has also vowed that it will not react with restrictive interest rate policy due to 'transient' increases in inflation.

"I would note that a transitory rise in inflation above 2 percent, as seems likely to occur this year, would not meet this standard."

As the year progresses, wholesale price increases will filter through to consumers, at which time we will enter the next chapter of our inflation experience. By then, our main question will likely have evolved from "How long will commodity/supply chain issues linger?" to "How sticky/permanent will consumer price increases be?"

Housing

It can be difficult to fully comprehend the devastating impacts that COVID and the accompanying shutdowns have had on economic activity around the world. For many families and businesses, the last twelve months have been the most challenging of their lives. Some areas of the economy, though, have thrived during the recessionary downturn. Perhaps none has been more impressive than U.S. housing. Fueled by an array of supply and demand tailwinds, home prices have surged over recent years. The median U.S. home price climbed from a pre-COVID level of $270,400 to $313,000 in February, even as home sales rose at a pace not seen since 2007.

Given fresh memories of a housing-sparked financial collapse, it's understandable that some view this latest boom with skepticism. Still, the dynamics of residential real estate have changed considerably since the mid-2000s, and trends driving the recent improvement in the industry could have lasting strength. Below, we'll outline a few of the forces helping to support the housing market in the U.S.

Demand

If you find yourself about as interested in the housing market as you have ever been, you are not alone. According to Google Trends, search interest in the term "homes for sale" has never been higher.

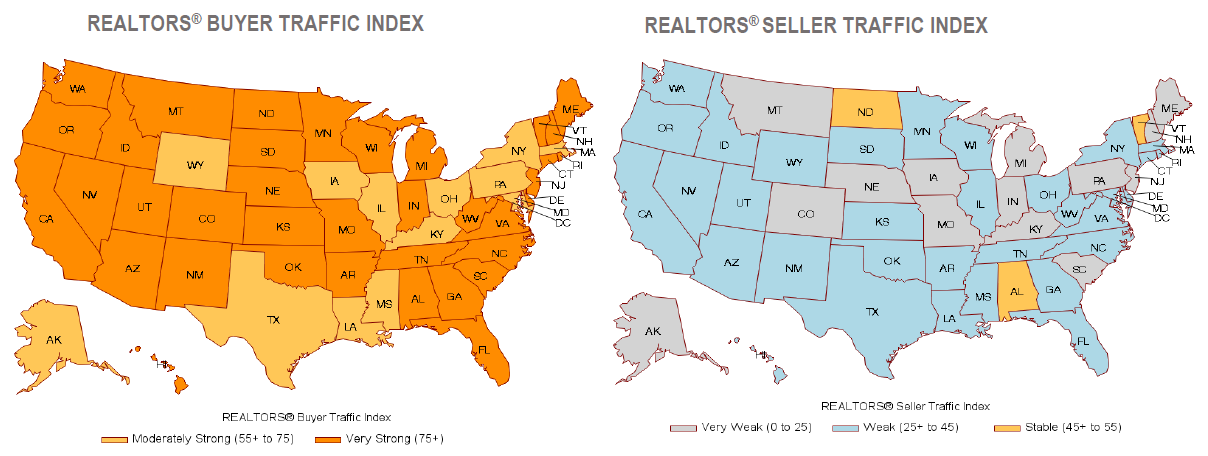

It should be no surprise that with search interest this high, buyers are in abundant supply. In any transaction, you need a willing buyer and a willing seller. However, a recent survey by the National Realtors Association showed a breathtaking mismatch in their estimates of Buyer/Seller willingness to seek a transaction.

So the market right now is full of frenzied buyers and unmotivated sellers. If there was ever a "seller's market" where newly listed homes are downright coveted, this is it. Although, that one little question of where you'll live might linger as you contemplate listing (more on that in the supply section).

The level of enthusiasm in housing is plain as day. It is apparent based on survey data, pricing trends, and even buyer's willingness to do things that seem downright crazy, like waiving contingencies/inspections or all-cash offers substantially above asking. Let's take a look at who these buyers are.

Most buyers are in or around their peak earning and child-rearing ages of 35-55 years old. That cohort also represents more than half of the U.S. population.

Buyers these days also have good or excellent credit. Note the magnitude of sub-prime originations (lower credit scores) in 2003-2007 versus today. Banks and mortgage companies simply are not offering mortgages to anybody with a challenged credit history or an inability to afford a hefty down payment (or mortgage insurance).

In addition to stricter lending standards, existing homeowners' financial positions are dramatically improved versus 2007-2008. The amount of leverage in the housing market (amount of outstanding debt versus the properties' value) is quite low. On average, Americans have over 65% equity in their homes. Significant equity positions are a stabilizing force for prices since folks that wish to 'move up' can use that equity as currency in a subsequent transaction.

Over the next 20 years, the aging of Millennials will be the main event on the demand side of the housing equation. Unprecedented levels of student debt and coming of age in a recessionary environment hampered Millennials' home ownership journey. But increasing rates of income and accelerating household formation clearly show a rising influence for this often-derided generation.

Some data related to homeownership and household formation has been rendered less valuable due to pandemic-related issues (statistical adjustments gone awry or outlier/base effects). But the trend toward homeownership and away from renting for younger Americans is undeniable.

The prospect of student loan forgiveness/relief is far too political for us to comment on in a quarterly newsletter.

But legislation seeking to unburden Americans of their $1.57 trillion in student loan obligations would almost certainly enable a new cohort of prospective home buyers.

Supply

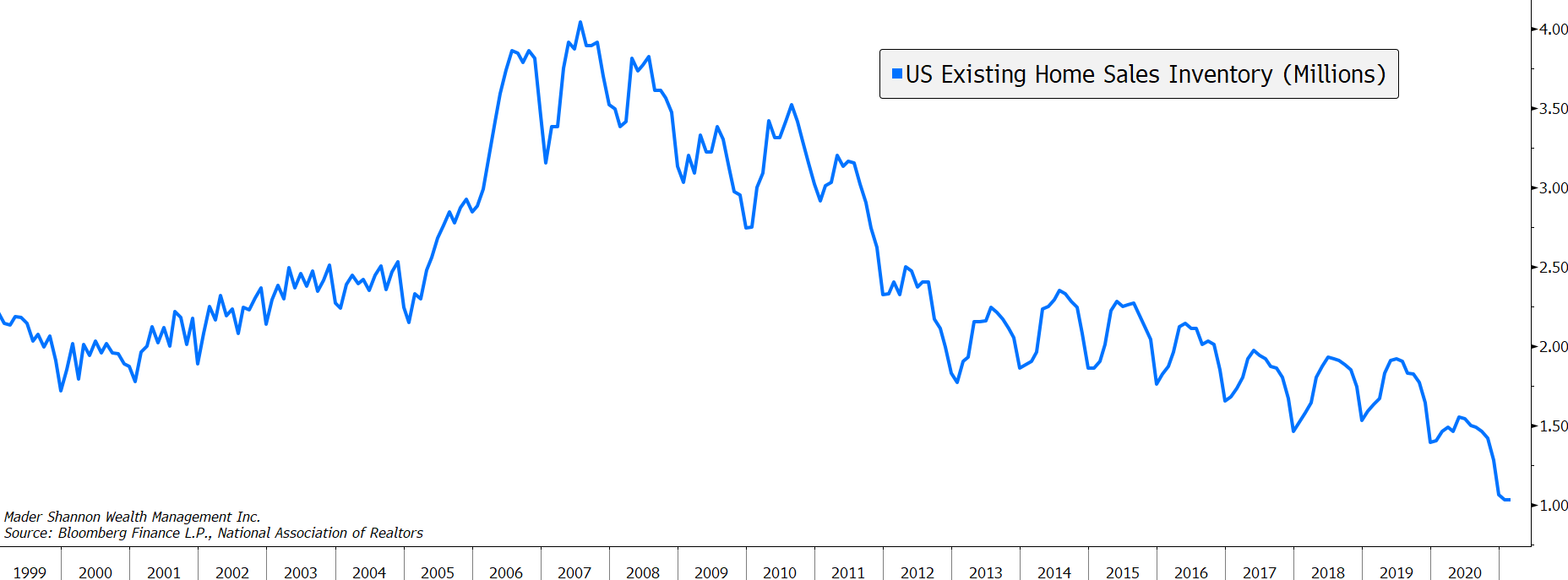

Single family housing supply has a simple problem: there isn't enough of it. The inventory of existing homes available for sale has been subdued for years, but it cratered to new lows in 2020. At current levels, there's only two months of supply available in the market – the lowest on record and less than half of what there's been in comparably healthy periods over the last 20 years.

Demographic trends are contributing to the scarcity. The heads of roughly 55% of all owner-occupied households in the U.S. are at or nearing retirement age, compared to only 41% in 1994. And for a substantial number of those households, the equity they've built is an important piece of their retirement plan. According to Census Bureau data, three-quarters of households aged 65 and older have home equity, but less than half own a retirement account. And for the average homeowner in that age group, home equity comprises nearly 70% of their net worth.

In years past, cashing out and moving to a senior community might have seemed an attractive option for some retirees. But in light of a pandemic that disproportionately targeted older generations – especially those living in close contact with others – that option has lost some appeal. Fortunately, they have alternative courses of action. Whether by opening a home equity line of credit, taking advantage of record-low interest rates with a cash-out refinance, or securing a reverse mortgage from the legendary Tom Selleck, retired homeowners have plenty of ways to access their home's equity. Unfortunately for inventory levels, that also means fewer retirees will leave their homes in the foreseeable future.

Adding to the supply shortage is a lack of new homes being built. New housing starts in the U.S. have been below the long-term average for the last decade. What's more, that average doesn't adequately account for continued population growth; a million new homes in 1960, when the population was 180 million, is quite different from a million in 2021, after the population has nearly doubled.

The solution to the supply shortage, it seems, is quite simple. We need to build more homes. As is usually the case, though, solutions are simpler in theory than in practice. When the housing bubble burst 15 years ago, the entire industry came face-to-face with financial ruin. The homebuilders and suppliers that managed to survive, rightfully scarred by the experience, vowed to take a more cautious approach to their businesses going forward. Production capacity dwindled.

Now, housing is back. According to industry veteran and D.R. Horton CEO David Auld, it's the best market he's ever seen. That means there's room to add capacity back, but rebuilding capacity takes resources, and right now, resources are in short supply. For one, qualified labor is hard to come by. While millions of Americans remain out of work, the headline unemployment rate has already fallen back to its long-term average, and job openings have fully recovered to pre-pandemic levels. Thirty-eight percent of construction firms in a March small business survey cited a shortage of qualified labor as their top business problem. Fifty-five percent said they had few or no qualified applicants for job openings.

Consequently, each of the large, publicly traded homebuilders anticipates increased labor expenses in 2021. The higher wages are intended to attract and retain workers, but it also puts upward pressure on home construction costs.

Material shortages have compounded cost pressures. Commodity prices, buffeted by supply chain issues and a year of consumption dominated by goods, rather than services, are at the highest level in years. For two key inputs to home construction, the cost increase has been especially pronounced. Copper prices have doubled in the last year. Lumber has quadrupled.

Somewhat concerned by cost uncertainties in the year ahead and unable to keep up with demand, several builders are deliberately slowing customer orders to ease construction backlogs. In some cases, they've chosen to raise prices until demand subsides. In others, they've refrained from releasing new lots for purchase. In any case, even if new homes can fill the supply gap, it would appear the prices of those homes are destined to be higher than in the past.