Happy New Year from Mader Shannon! We hope your 2022 is off to a prosperous start.

Frequently in markets, calendar dates like quarter-end and year-end can act as inflection points in which risk appetites and investment rationales are reassessed. The first few weeks of this year have so far conformed to that tendency. Given that, we thought it worthwhile to present you with a broad review of the US economic position.

We feel fortunate for the strong run our strategies have had over the past few years, and we’re looking forward to the unique challenges and opportunities that 2022 may offer. We’re always eager to share thoughts about positioning, strategy, and investment philosophy. Please let us know if you’d like to set up a portfolio and/or account review.

Kyle

Scene Setting – Economic Fundamentals

The past two years have presented extremes of every kind in economic data. To move past the noise, let’s review some indicators in bulk and ask the simple question: Are we doing better now than the long-term average?

We’ve chosen to use the 20-year average for each indicator. The past 20 years saw the rise of the internet, a housing boom/bust, a pandemic, and some of the most prosperous years the United States has ever seen. So, how are we doing now?

The economic picture is bright. Whether it’s manufacturing, retail sales, unemployment, wage growth, or even capital spending, every activity indicator is outperforming its long-term average. Of course, you’ll likely note the one outlier at the bottom of the table – inflation.

We’ve already spilled a great deal of ink when it comes to inflation, but as the most popular/controversial economic theme going right now, we can’t help but dive in yet again.

At the end of 2020, we noted that the pre-conditions for a “post-war” style bout of inflationary pressures had likely been met (fiscal stimulus, pent-up demand, and supply chain bottlenecks). Mid-year 2021, we noted that global supply-chain forces were pushing prices higher for select consumer items in a dramatic fashion, but that the advance was still in a narrow group of goods. We wondered how sticky those increases would be and whether they would permeate other areas of the economy. Most of the economic forecasting community expected those pressures to be ‘transitory.’

As we assess the situation in the first month of 2022, there is little doubt that price pressures have broadened into other areas of the economy. Let’s review the long-term trajectory of producer and consumer prices. Remember, these indices represent an annual rate of increase, not an absolute price level.

Over the past 50 years, we’ve seen at least a half dozen dramatic spikes in producer prices. Yet, only three of those instances (1974/1980/2021) translated to a commensurate rise in consumer prices. Widespread adoption of productivity-enhancing technology and the development of global supply chains in the 1990s and early 2000s are generally credited with keeping consumer inflation at bay over the past 30 years.

The producer pricing surge post-financial crisis was accompanied by radically new monetary policies that brought fears of 1970s-style consumer price rises, but inflation never came. Why? Likely because consumers were trapped in a deleveraging cycle with high unemployment, and they couldn’t afford to chase goods and services like they otherwise might prefer.

The COVID experience brought together the force of central banks’ powers and governments’ fiscal spending – a phenomenon we dubbed ‘Policy Coordination.’ That joint effort put money in people’s pockets and kept interest rates at low levels. In conjunction with crippled supply chains, that combination pushed inflation to rates that more than half of all Americans have never seen in their lifetime.

So, that’s where we are – economic growth is at least as good, if not better than pre-COVID levels, but with a persistent inflationary backdrop.

The next question must be: How much longer/higher can prices rise? Let’s review the major categories within the consumer price index.

The past five years offer a window to decompose both pre-pandemic and current inflationary trends. You’ll note that price inflation in services historically has been relatively stable and the main driver of prices (blue bar). In contrast, goods inflation (orange bar) has typically not contributed much to inflation – until now.

The rise in goods prices has stemmed from a surge in demand for durable goods and a supply chain that was never designed for such rapid fluctuations.

One measure of supply chain chaos is the cost of moving goods from one point to another, and those costs are always passed on to the end consumer. We’ve all heard about the turmoil at ports, but how about interstate trucking?

Freight transportation costs are increasing by nearly 18% per year!

We’ve never seen cars in such short supply in this country. Shortages in the most basic semiconductors, manufacturing shutdowns, and a shift from public transit towards passenger cars have rocked the auto industry.

As you’ve likely heard, prices have increased dramatically in response to the supply/demand picture. Those higher prices have more than made up for any sales shortfalls, as used car prices rose more than 60% in the last two years.

How about the demand side of things? Let’s look at a few examples of industry-specific retail sales data.

Consumers have shifted their eating preferences to ‘at home’ at a rate of +31% in just two years. That is a significant demand shock for one of our economy’s ‘boring’ industries that grew at just 6.4% yearly from 1994 to 2019.

What about the big-ticket household items? How about an increase of over 30% in two years!

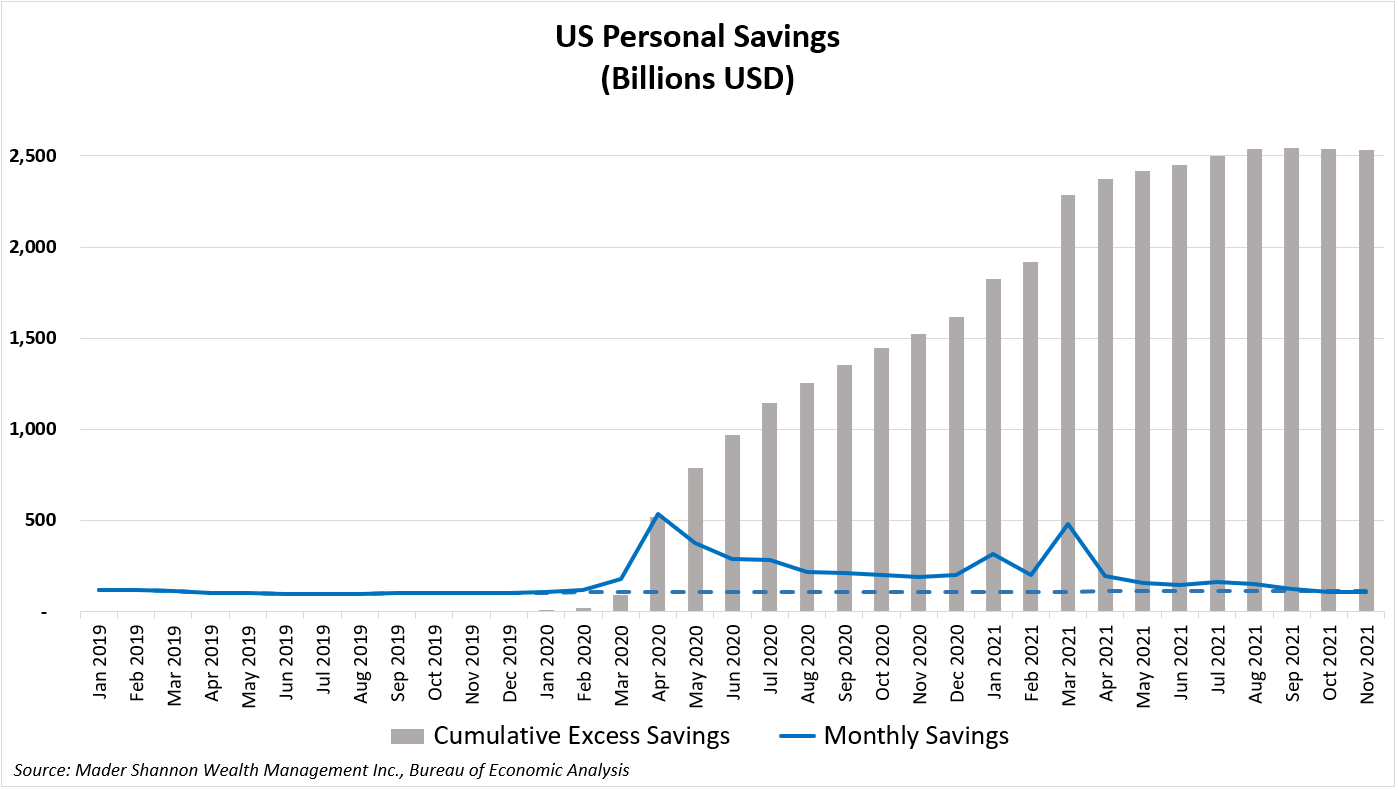

So, how do we get out of this inflationary predicament? Unfortunately, it’s going to take time. Consumers need to spend down their savings, and supply chains need to heal. But most importantly, it will take time for competition, productivity, and demographic trends to reassert their disinflationary powers.

Economic forecasts range from a normalization of inflation rates to under 3% by year-end 2022 or an accelerating wage-price spiral that will persist for years to come. Although if you feel a sense of apathy towards the economic forecasting community, we wouldn’t be surprised.

As inflation dynamics continue to shift, we will remain hyper-focused on companies’ abilities to grow their top lines, pass along higher input costs, and retain their margins. After all, inflation impacts each economic entity differently - your higher prices are somebody else’s higher revenue.

What to Watch in 2022

Corporate Earnings

The ability of large corporations to effectively pass on all the increases in input costs was the main story for the equity markets in 2021. Profit margins for S&P500 companies ended the year at record highs. Although to be fair, several secular trends and accounting abnormalities have contributed to margin expansion over the past two years.

Eventually, personal savings will be depleted, and consumers will be unable to absorb pricing initiatives. But there are very few signs that we’re imminently approaching that point based on current data. Consumers still have a war chest of savings to draw from in the aggregate.

The next few weeks will be the busiest of the 4Q2021 earnings reporting season. We anticipate that the market will punish companies who flag margin compression or unmanageable wage expense growth. Our focus, as always, will be to identify the companies that are/are not effectively managing in this challenging environment.

Central Banks

The Federal Reserve and many other global central banks find themselves in a favorable position on one mandate (employment) and wildly out of sync with another (price stability). For that reason, many central banks over the past six months have begun to raise rates. And the United States Federal Reserve has made four incremental messaging changes to prepare markets for higher interest rates.

The QE taper was initiated and sped up (end date in March). Rate hike expectations have been pushed from 1-2 to 3-4 rate hikes expected in 2022 (ending 2022 at about 1.00%). And balance sheet runoff has been floated as potentially beginning this year.

The policy shifts thus far have merely returned interest rates to a path of normalization. Monetary policy is still far from being in a restrictive posture. Remember, pre-pandemic; the federal funds rate was 2.50% (currently 0.00%), and the balance sheet was $4.0 trillion (now $8.4 trillion).

Day-to-day messaging will always impact stock and bond markets, but the very fact that the messaging exists is proof of policymakers’ anxiety around disturbing financial markets.

If the mode of operation changes to abrupt action without forewarning, that would mark a troubling shift in the environment for interest rates, equity valuations, and potentially economic growth. Thus far, there are no signs of any willingness by central bank leadership to take such a confrontational approach – but that’s the risk.

Politics

Given present polling, it appears unlikely that the Democrats will retain both houses of Congress after the midterms this fall. The Build Back Better bill could have one last push in the spring/summer, albeit as a much less ambitious package. The outlook for any significant bipartisan legislation looks to be dim for the remainder of 2022 and possibly through 2024.

We won’t wade into any personal predictions or preferences, but we will share an old favorite chart that has graced the pages of newsletters past.

The spread between how republicans and democrats view the world is, unsurprisingly, vast. Interestingly, it’s about as wide as it was right before the election in 2016.

Historically, markets have done well in gridlock. The idea goes that if the “rules of the game” are set and unlikely to change, businesses can plan and execute their initiatives more effectively. On the other hand, for markets that have grown accustomed to a ‘policy coordination’ world, no longer having fiscal policy as an implicit backstop could be an unwelcomed status quo.

The Next Expansion

After the economic collapse of 2020 and the encouraging rebound in 2021, we can’t help but contemplate what this new economic expansion might hold. The past three expansions were unique in the history of the United States. They were marked by low/falling inflation, low/falling interest rates, and remarkably steady GDP growth.

Is it reasonable for us to expect another such expansion? As the year unfolds, we look forward to sharing our thoughts.

Thank you for taking the time to review our note; we hope you enjoyed it. If you have any follow-up questions, please let us know.