Week in Review

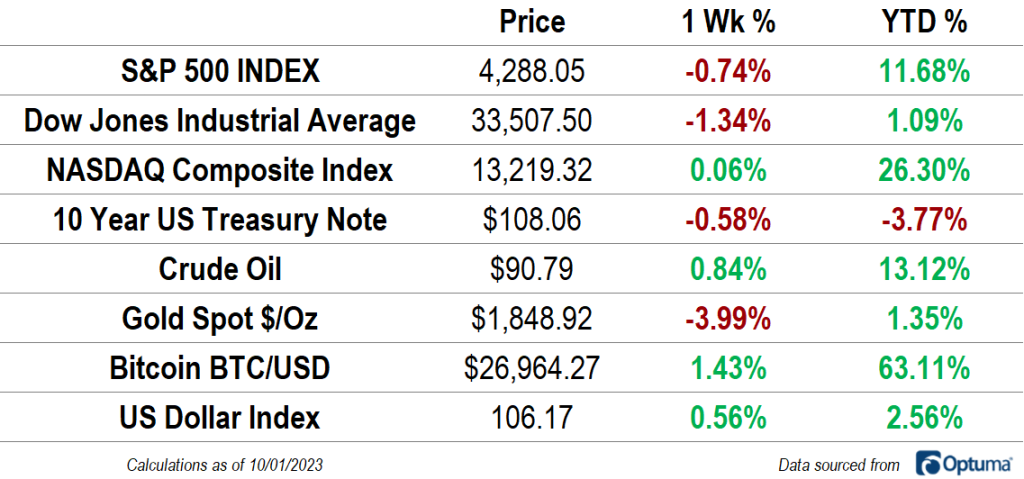

The NASDAQ Composite managed to close higher last week, ending its lowing streak at 3. The Dow Jones Industrial Average wasn’t quite so lucky. It dropped 1.3%, bringing its year-to-date gain to just 1.1%. The US Dollar Index rose for the 11th straight week, only the second time in the index’s history that we’ve seen that feat. Next week, we’ll try to match the record set back in 2014. Interest rates continued to rise as well, with 5, 10, and 30-year Treasury yields all reaching their highest levels in more than a decade. Gold dropped 4% – it’s worst weekly performance in more than 2 years – and oil prices continued to drift higher.

Stocks lived up to (or in this case, down to) their seasonal reputation in September. Over the last 70 years, September has been the worst month for the S&P 500 index, resulting in an average decline of 0.6%. This year, the index fell 4.9% for the month. Ready for the good news? The fourth quarter is is typically the best of the year. Since 1950, stocks have risen 4.2% on average in Q4.

Relatively Speaking

For the second month in a row, only one sector managed to end in the green. It was Energy, once again. The Energy sector rose 3.2% over the past month, outpacing a 4.7% decline for the benchmark index. Losses were led by the Real Estate (-8.2%), Utilities (-7.2%), and Industrials (-6.1%).

Growth sectors are still in the pole position year-to-date, with Communication Services, Information Technology, and Consumer Discretionary each up more than 25% since December. Investing in any other area would have yielded a return well below that of the S&P 500’s 11.7% YTD gain. Risk-off groups are all down for the year, paced by a 16.5% drop in the Utilities sector.

What’s Ahead

Here are the key data releases and events to keep on eye on in the coming days.